Programs like ScholarShare 529 and California Kids Investment and Development Savings Program (CalKIDS) are designed to help build education savings over time. Some children may already have access to free scholarship accounts through CalKIDS without their households realizing it.

California has opened approximately 5.6 million CalKIDS accounts for eligible children and students. As of April 2026, about 900,000 children had claimed their accounts, meaning many eligible accounts may still remain unclaimed.Take a few minutes to check eligibility and access education savings funds that may already be available to you or a child/student you know. Read more below.

What Is ScholarShare 529?

A 529 account is a type of education savings account that can help individuals and households set aside money for future education expenses. These accounts are commonly used for college costs, but they may also be used for certain vocational programs, trade schools, and some K–12 educational expenses. When funds are used for qualified education expenses, earnings and withdrawals are generally tax-free.In California, the state’s official 529 college savings plan is called ScholarShare 529. Accounts can be opened or contributed to by a wide range of supporters, including relatives, friends, and others.

What Is CalKIDS?

California also offers a related program called CalKIDS, which provides eligible children with scholarships from the State of California to help them begin saving for future education expenses. The CalKIDS account holds money provided by the state, while the ScholarShare 529 account allows money to be added and grow their own savings over time. Although CalKIDS and ScholarShare 529 are separate programs, both are used best when connected together.

How Do 529 Account Balances Grow?

In addition to any free seed money the state might provide, there are two ways 529 accounts grow over time:

- Contributions you or others make to the account, including additional funds that may be available through programs offered by some cities, counties, and community organizations

- Investment returns, which are not guaranteed and can change depending on market conditions

ScholarShare 529 offers a variety of investment portfolio options designed for different comfort levels and savings goals. Some options focus more on stability and lower risk, while others involve more risk but may provide greater growth potential depending on market conditions. Similar to retirement accounts like a 401(k), 529 accounts allow account holders to choose from different investment approaches based on what feels right for their situation and goals. You can review ScholarShare 529 investment performance and portfolio information here and compare investment portfolio options here.

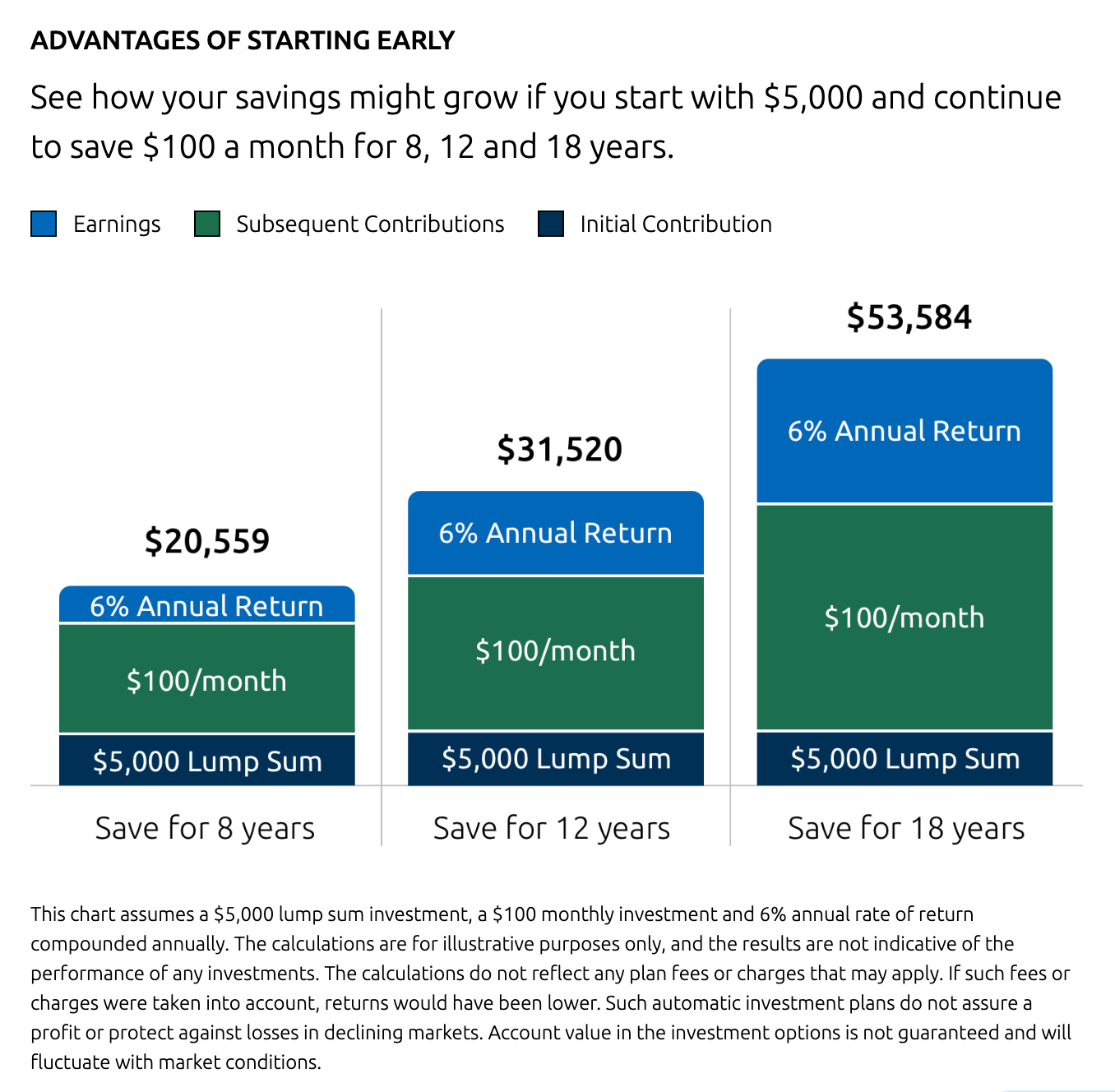

The earlier you begin saving in a 529 account, the more time there is to build more savings.

Image credit: Scholarshare529.com

How Is a ScholarShare 529 Account Different From a Typical Savings Account?

While there are different savings account options available, such as bank saving accounts, ScholarShare 529 accounts are designed specifically for education savings and offer additional benefits, including:

- Tax-deferred growth and tax-free withdrawals when funds are used for qualified education expenses (tuition, housing, computers, internet access, books, vocational or trade school costs, and some K–12 educational expenses)

- No income restrictions to open an account

- A variety of investment portfolio options, including lower- and higher-risk options based on different comfort levels and savings goals

- A maximum account balance limit of $529,000 per beneficiary

ScholarShare 529 accounts are generally considered more financial aid friendly than some other ways of saving for education because of how these accounts may be considered during the financial aid process. It’s important to note that how savings are counted can vary depending on who owns the account and the policies used by a particular school.

For example, savings held in a parent-owned 529 account are generally counted differently during federal financial aid calculations than money held directly in a student’s name. Typically, up to 5.6% of savings in a parent-owned 529 account may be considered when determining financial aid eligibility, while student-owned assets may be counted at a higher rate, sometimes 20% or more. Beginning with the 2024–2025 FAFSA, withdrawals from grandparent-owned 529 accounts are no longer required to be reported on the FAFSA and generally do not negatively affect federal financial aid eligibility. Checking with the schools you are considering can help you better understand how education savings may affect financial aid eligibility.

ScholarShare 529 offers a variety of investment options and lower investment expenses compared to many other 529 plans. There are no sales charges, startup fees, or annual maintenance fees associated with ScholarShare 529 accounts. There are investment fees, which vary depending on the portfolio selected.

Some cities, counties, and community organizations across California may also offer local incentives connected to ScholarShare 529 accounts. See if your community offers any ScholarShare incentives here.

Who Can Open or Benefit From a ScholarShare 529 Account?

ScholarShare 529 accounts can be opened by parents, grandparents, other family members, family friends, financial professionals, scholarship funds, or other entities. To open a ScholarShare 529 account, the account owner must have a valid Social Security Number (SSN) or Taxpayer Identification Number (TIN). The beneficiary of the account — including a child, family member, friend, or even yourself — must also have a valid SSN or TIN.

This means a parent or caregiver without an SSN may still be able to open or contribute to an account for a child who has an SSN or ITIN through another eligible account owner. Learn more here.

Ready to Get Started?

Whether you are starting early, exploring options for your child, or simply learning more about education savings programs, understanding the resources available can help you decide what works best for your situation.

Visit ScholarShare529.org today to learn more!

Knowledge Check

Let's do a quick knowledge check on 529 accounts!

Consider Creating a FREE Account!